MORTGAGE SECURITIZATION AND APEX MORTGAGE DISCHARGE REPORT WESTPACK MORTGAGE

19TH June 2026

The contemporary intersection of international tax administration, structured corporate finance, and real property jurisprudence requires an exceptionally rigorous forensic framework to identify the true beneficial owners of securitized debt instruments. 1 The modern global financial system operates not merely as a marketplace for the localized exchange of physical assets, but as a highly sophisticated, multi-layered administrative trust managed predominantly by the United States Department of the Treasury. To fully comprehend the legal mechanics of mortgage discharges executed via U.S. Treasury ledger reconciliation— specifically concerning the estate of R Angelo R and Carmela R, Westpac Banking Corporation, and the systemic clearing registries managing the underlying debt—it is imperative to first deconstruct the ontological nature of credit origination and the administrative scaffolding upon which modern debt obligations are constructed.

This research report delivers an exhaustive, step-by-step reconstruction of the administrative and commercial mechanisms governing the R mortgage dispute, functioning as the primary forensic analysis to be utilized in both the domestic courts of Western Australia and the United States District Court for the Southern District of New York (SDNY). The evaluation establishes that Westpac Banking Corporation, acting in corporate coordination with JP Morgan (Australia) Limited, Perpetual Trustees, and Waratah Receivables Corporation, is highly unlikely to possess standing as the actual creditor or the Holder in Due Course (HDC) regarding the residential mortgage instruments executed by the primary mortgagors. Using a specialized fiduciary framework, this analysis demonstrates that Westpac operates entirely as a servicing nominee and withholding agent rather than a bona fide creditor advancing substantive corporate capital.

The Jurisdictional Shift of 1933 and the Usufruct Credit Paradigm

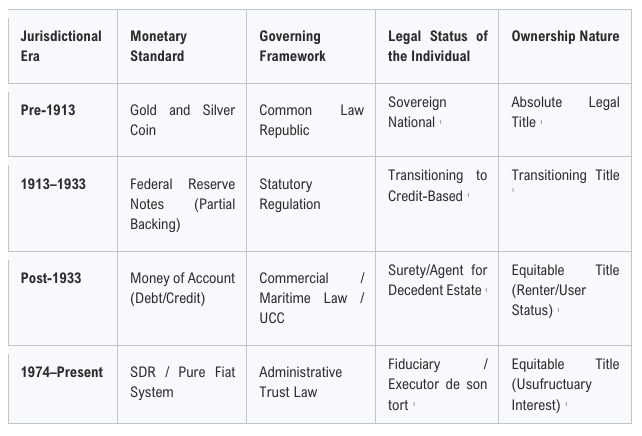

The contemporary banking system does not operate under the classical fractional reserve model where financial institutions act as intermediaries lending out pre-existing customer deposits. Instead, the modern global financial system operates upon a credit-based system of "discharge" governed predominantly by maritime trust law, the Uniform Commercial Code (UCC), and the Law of Agency. This transition away from a substance-based monetary standard was legally codified in the United States by the formal insolvency reorganization of the United States federal corporation in 1933. Consolidated under the Emergency Banking Act of March 9, 1933, and permanently established into public policy by the passage of House Joint Resolution 192 (HJR 192) on June 5, 1933, the global commercial architecture underwent a permanent, irreversible paradigm shift.

HJR 192 fundamentally altered the nature of global commerce by indefinitely suspending the gold standard and the requirement that domestic and international commercial obligations be payable in substantive, intrinsic assets. The legislation explicitly declared that the requirement to pay debts in gold or any specific coin was contrary to public policy, effectively removing physical commodity-backed consideration from private circulation across the interconnected global banking syndicate. Within this closed-loop fiat paradigm, commercial obligations are no longer "paid" in the traditional sense of a final settlement involving a physical commodity possessing independent, intrinsic value; rather, they are "discharged" against a centralized ledger maintained by the administrative state.

Federal Reserve Notes and their international equivalents circulate strictly as debt obligations of the U.S. Treasury utilized to balance ledger entries on the commercial board. Money functions strictly as a "money of account," a debt-based accounting unit utilized solely to track and balance ledger obligations across international boundaries and institutional balance sheets. Because the requirement to pay in substance was permanently suspended by statutory mandate, the productive capacity, future labor, and human credit energy of the living populace serve as the primary source of value and the ultimate collateral backing all national and global debt obligations.

Through the registration of birth records and the issuance of identification numbers, the state establishes a "decedent estate" or a corporate debtor construct on government ledgers. The modern legal system does not interact with biological matter; it interacts with "persons," a term defined by statutes to include bodies corporate or unincorporate. When a statute imposes a tax, a regulatory fine, or a debt on a "person," it targets the artificial entity created by the registration of a birth. The living individual is presumed, by default, to operate merely as the subordinate agent and liable surety for this bankrupt corporate debtor, holding only a conditional equitable title to their assets while the administrative state or its institutional nominees retain ultimate legal title as the bankruptcy trustee. In this specific commercial framework, localized property obligations—including income taxes, property taxes, and mortgage payments—are structurally defined as administrative rent payments made to the trustee for the privilege of utilizing collateralized assets on the commercial ledger.

The foundation of modern corporate law, established in the landmark case Salomon v A Salomon & Co Ltd, dictates that an artificial person is a distinct legal entity from its human controllers. While this principle was originally designed to protect humans from corporate liabilities, the administrative state inverts it, utilizing the separation to create a liability-bearing construct and then attaching those liabilities to the living human via presumed agency. To navigate this reality, fiduciaries must understand that operating under the presumed status of a retail debtor traps the individual in a system of perpetual liability, necessitating a strategic shift to a creditor-fiduciary posture to reclaim jurisdictional autonomy.

Read More >>