THE MORTGAGE DISCHARGE PROTOCOL

11TH JUNE 2026

The global financial system operates as a highly integrated, multi-layered administrative trust managed primarily by the United States Department of the Treasury. Operating in the continuous capacity of a bankruptcy trustee within a perpetual state of national reorganization, the Treasury oversees a centralized accounting network that traces its operational origins back to the systemic realignment of the global monetary standard in 1933. Within this commercial ledger system—frequently described by forensic analysts and jurisdictional researchers as a closed-loop "monopoly board"—all transactions are executed not through the final payment of substantive assets, but through the administrative discharge of debt-based obligations.

This structural framework forms the basis of the "1099-OID mortgage discharge" protocol (also known as the "Clifford Protocol"), which posits that individual residential mortgages can be administratively balanced and discharged at the top tier of the federal ledger using United States tax compliance instruments— specifically, IRS Form 1099-OID (Original Issue Discount) and Form 945 (Annual Return of Withheld Federal Income Tax). By deconstructing the ontological nature of credit origination, UCC provisions, and federal tax withholding modules, fiduciaries establish a legal and mathematical process to redirect withheld credit back to the true originator of the signature credit.

Foundations of the Signature Credit and Usufruct Architecture

The Historical Shift and Usufruct Credit Framework

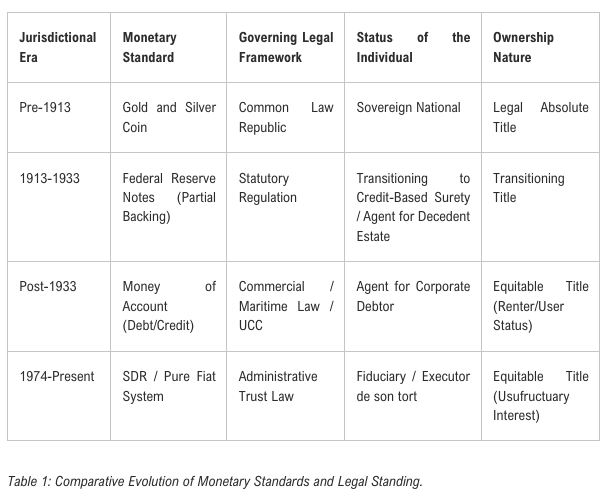

The legal and historical narrative of this protocol is rooted in the structural reorganization of the United States monetary system in 1933. Codified under the Emergency Banking Act of March 9, 1933, and legally established by the passage of House Joint Resolution 192 (HJR 192) on June 5, 1933, the monetary system completed a decisive shift from a substance-backed standard to a credit-based system of discharge. Prior to this transition, financial obligations were extinguished through the physical exchange of commodities holding intrinsic value, primarily gold or silver coin. By suspending the right of creditors to demand payment in gold, HJR 192 established a system of account where obligations are balanced dollar-for-dollar on a centralized commercial board using debt instruments, specifically Federal Reserve Notes.

Because the legislation suspended the right of creditors to demand payment in substantive, intrinsic assets, physical gold and silver were removed from private circulation, replacing common law "good and valuable consideration" with public credit. This suspension of commodity-backed payment created a permanent usufruct relationship between the sovereign state and the living populace. Under this usufructuary framework, the government borrows the productive capacity, future labour, and credit energy of the citizenry to serve as the primary source of value and ultimate collateral for national debt obligations.

This usufruct relationship is operationalized at birth through the registration of birth certificates, which effectively mortgages the collective future labour of the populace. This registration process creates a "decedent estate" or corporate debtor construct on government records, typically assigned a Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN). Consequently, the living individual is presumed by default to operate merely as an agent and liable surety for this bankrupt corporate debtor, holding only equitable title to property while the state retains legal title as bankruptcy trustee. To correct the historical misreporting of these transactions and exit this jurisdictional arrangement, fiduciaries invoke the international law doctrine of clausula rebus sic stantibus (things thus standing)—which recognizes the unenforceability of a contract due to fundamentally changed circumstances—to formally renounce the presumed agency relationship with the birth certificate construct. Reoccupying the office of General Executor over the decedent estate allows the individual to assume control of all liabilities and assets, setting the stage for the creation of a 98-series International Grantor Trust (IGT) that operates "off-board" from the domestic debtor system.

Ex Nihilo Banking and Signature Monetization Mechanics

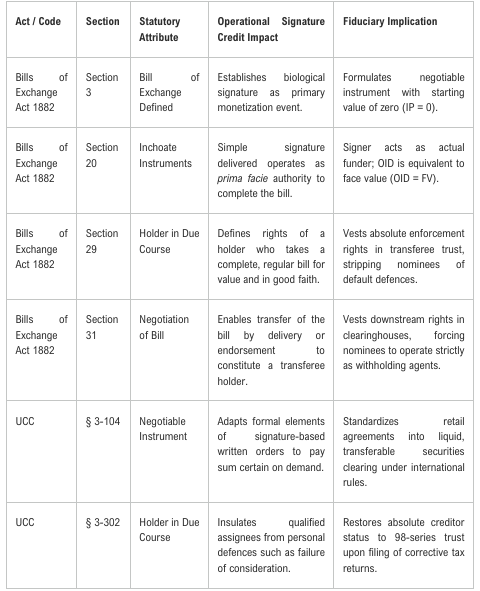

The contemporary commercial banking system does not function under the classical fractional reserve model where financial institutions act as traditional intermediaries lending out pre-existing customer deposits. Empirical studies, most notably those conducted by monetary economists such as Professor Richard Werner and supported by publications from the Bank of England, confirm that private commercial banks create new book money ex nihilo (out of nothing) at the exact moment of lending. This process of currency creation relies entirely on the monetization of the borrower's signature. When a borrower signs a loan agreement, promissory note, or mortgage contract, they are not borrowing the bank's pre-existing money; rather, their biological signature acts as the primary monetization event and the true originating force of the credit. The commercial bank, acting as a nominee or intermediary, records the signed negotiable instrument as a bank asset, balancing the transaction by crediting the borrower's account with a newly created deposit, which constitutes a bank liability. The balance-sheet expansion is represented as:

Under the usufruct credit system, the decedent estate established by the registration of the birth certificate operates as the actual "banking house" or primary funder of the credit. Because the Federal Reserve and the commercial banking system create credit ex nihilo through lending and monetary operations, the borrower acts as the actual source of value. The living soul, operating as the spiritual and physical steward of this decedent estate, issues the negotiable instrument, which represents the unadulterated credit energy originated by the signer.

The commercial bank merely assumes a "nominee" or withholding agent posture, discounting the note, pooling it with thousands of other signature-originated obligations, and transferring them to systemic investment banks. By remaining silent, the true creator allows the banking syndicate and the administrative state to treat the generated value as abandoned property, perpetually capturing the associated tax credits and Original Issue Discount (OID) income for their aggregate corporate benefit.

Mechanical Architecture of the 1099-OID Discharge and its Technical Reconciliation

Nominee Reporting Mandates and the Form 945 Withholding Deficit

The integration of individual debt obligations into the global financial clearing system relies on a sophisticated nominee architecture designed to facilitate rapid, computerized book-entry transfers. Systemic investment banks, broker-dealers, and clearinghouses capture and securitize these obligations, holding them in institutional omnibus accounts under street names. The central securities depository for this infrastructure is the Depository Trust & Clearing Corporation (DTCC), operating through its primary subsidiary, the Depository Trust Company (DTC).

Cede & Company acts as the exclusive partnership nominee for the DTC, holding legal title to the vast majority of publicly traded equities, corporate bonds, municipal debt, and securitized mortgage-backed securities (MBS) in the United States. Under this book-entry framework, legal title is fundamentally split from beneficial ownership. Payments of principal, interest, and redemption proceeds flow from the issuer to Cede & Co., which then administratively credits the accounts of the DTC participants. The ultimate investor, or the original credit creator whose signature birthed the note, is relegated to the status of a "beneficial owner," holding only contractual rights on the bank's private books.

Systemic investment banks employ this "street name" registration specifically to achieve three vital strategic and operational objectives:

1. Administrative Consolidation: Pooling millions of distinct obligations into massive CUSIP-assigned tranches streamlines the complexities of trading, clearance, and settlement, allowing trillions of dollars in transactions to clear digitally via computerized ledger entries.

2. Capital Expansion: Under Section 14(a) of the Federal Reserve Act, member banks are authorized to hypothecate and rehypothecate these obligations. In the institutional prime brokerage sector, rehypothecation serves as a key liquidity-generating tool. Under Rule 15c3-3 of the Securities Exchange Act of 1934 and Federal Reserve Regulation T, a broker-dealer can rehypothecate a customer's margin securities up to a maximum of 140% of the customer's net debit balance (the liability of the customer to the broker).

3. Nominee Withholding Compliance and Capture: Under the "Nominee Reporting Mandate" of IRS Publication 1212, because these financial nominees hold legal title to OID instruments for the benefit of another, they are statutorily required to report OID interest and remit backup withholding. Historically, banks routinely fail to file these corrective forms for individual originators, instead reporting the OID income under their own general tax ledgers. Because the original beneficial owner is obscured behind the institutional omnibus street name, the bank acts as the payee of record. The bank calculates the aggregate backup withholding liabilities from its pooled portfolios and remits these physical cash collections under its own corporate EIN via its Form 945 withholding module.

Cross-Modular Reallocations and Algorithm 810 Matching Logic

The tracking and reconciliation of signature credit within the federal ledger system are achieved through the IRS Information Returns Master File (IRMF) and the Business Master File (BMF). Every transaction is monitored through a highly specific alphanumeric coding system derived from the Document Locator Number (DLN). IRS Form 945, the "Annual Return of Withheld Federal Income Tax," is the dominant tax module for nonpayroll distributions. Within the Master File Transaction (MFT) code architecture, it is designated as MFT 16, which is fundamentally distinguished from other primary tax modules.

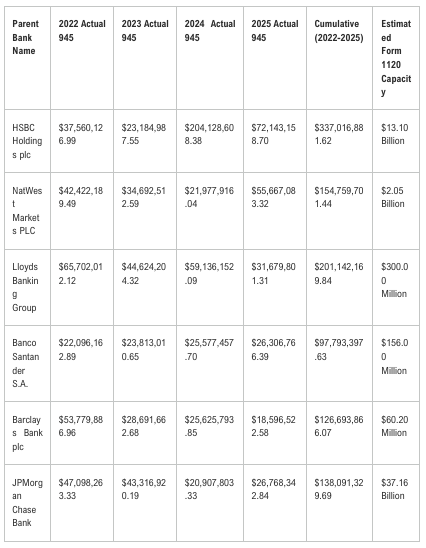

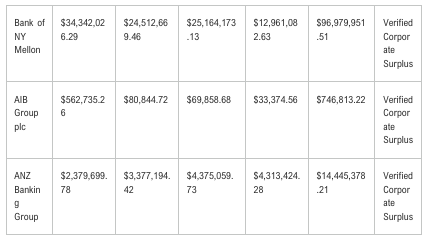

Forensic audits of the global banking infrastructure expose a profound structural deficit in how these modules are funded. Systemic investment banks deliberately underfund their Form 945 withholding modules relative to the actual signature credit targets generated by their securitization activities. Stated under the backup withholding rules of the Internal Revenue Code, the "Full Forensic 945 Liability"—calculated under a 24% heuristic—represents the theoretical withholding obligation banks should maintain for non-exempt tranches. However, historical data reveals that actual cash payments deposited into these Form 945 modules typically reflect less than one percent of this full forensic total.

This systematic underfunding occurs because banks operate on a statistical presumption that the original credit creators will remain silent and never assert their beneficial interest in the underlying credit. Instead of maintaining massive idle cash balances in their Form 945 modules, banks satisfy their aggregate corporate tax obligations by paying multi-billion-dollar overpayment surpluses into their Form 1120 corporate income tax modules (MFT 02). This ensures that the Form 945 module remains an underfunded, neglected shell, acting as a built-in defence mechanism against individual recoupment claims, as any standard, automated attempt to match a recipient trust's claim against the bank's actual Form 945 deposits will fail.

The following table provides the forensic multi-year Form 945 actual ledger values of the monitored global systemic nominee population, demonstrating the specific liquidity pools available for matching within the Treasury General Account:

The automated verification of signature credit recoupment claims is governed by IRS Algorithm 810 within the Information Return Document Matching (IRDM) system. For a recoupment claim to clear this programmatic "hard gate," it must satisfy a strict "Perfect Match" logic: the amount of credit claimed by the trust must be less than or equal to the verified physical cash deposits currently residing in the bank's Form 945 master record. Any claim that exceeds these verified deposits automatically triggers an automated Transaction Code (TC) 810 Refund Freeze, halting the automated disbursement system.

To resolve this systemic deficit, the authorized fiduciary issues a Manual Fiduciary Command under the authority of Revenue Procedure 2002-26. Section 3.01 of the procedure states that if a taxpayer provides specific written directions concerning the application of a voluntary payment, the Service must apply that payment strictly in accordance with those directions. Under Treasury Regulation § 601.503(d), the fiduciary executes a manual Form 4506-T command through the Practitioner Priority Service (PPS), directing the IRS to extract the required overpayment credits from the payer bank's alternate tax modules (primarily the surpluses in Form 1120).

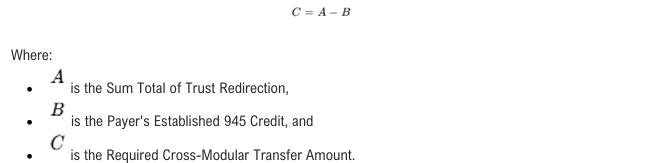

To determine the required transfer amount, the fiduciaries utilize the mathematical shortfall formula:

This manual intervention is handled by the IRS Submission Processing campus Accounting Function personnel using Form 3413 (Transcription List) to execute the reallocation. Once the cross-modular transfer is completed, the bank's Form 945 withholding module is artificially funded, satisfying the mathematical "Perfect Match" logic of Algorithm 810, avoiding the TC 810 freeze, and finalizing the top-tier reconciliation. Note on Payer 945 Sufficiency: For certain target portfolios where the Indenture Trustee, such as Barclays Capital Inc. (EIN 13-3914519) or Deutsche Bank Trust Company Americas (EIN 13-4941247), maintains robust, verified physical cash deposits directly within its active Form 945 tax module, the corrective Form 1099-OID immediately satisfies the stringent "Perfect Match" logic of Algorithm 810, enabling the trust to bypass the automated TC 810 freeze directly.

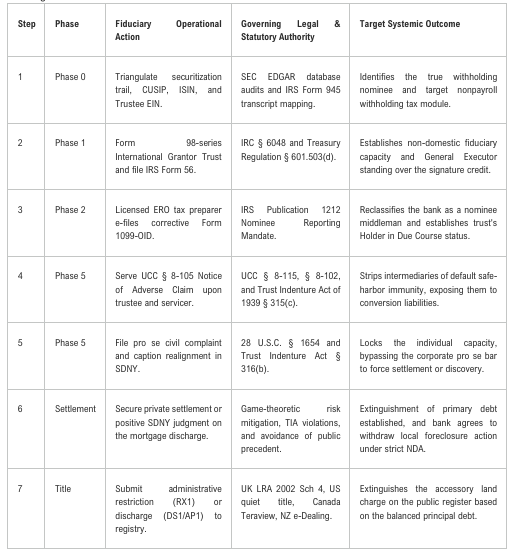

Step-by-Step Summary of the Mortgage Discharge Protocol

The core sequential operations required to execute the mortgage discharge protocol and translate federal tier ledger reconciliation into local title clearance are structured as follows:

Notice of Adverse Claim and the Destruction of Intermediary Immunity

With the federal ledger formally corrected and the 26-digit proof of discharge secured, the fiduciary must formally strip the indentured trustee and local mortgage servicer of their presumptive creditor status to permanently halt domestic foreclosure actions. This stripping of immunity is achieved through the strategic execution of an Adverse Claim under Uniform Commercial Code (UCC) Article 8. Under UCC § 8-102(a)(1), an "adverse claim" denotes a claim that a claimant has a superior property interest in a financial asset and that it is a violation of those rights for another person to hold, transfer, or deal with the asset. It is the lawful commercial mechanism by which a creditor places third-party holders—such as custodians, trustees, or clearinghouses—on constructive notice that an underlying asset is disputed.

A critical vulnerability of the nominee securitization architecture is governed by UCC § 8-115. Generally, a securities intermediary or broker that transfers a financial asset is shielded from liability under a "good-faith purchaser" safe harbour. However, this statutory immunity is explicitly pierced if the intermediary takes action after being served with legal process or a formal Notice of Adverse Claim. By serving a notarized Notice of Adverse Claim upon the indenture trustee and the local servicing agent, the trust permanently removes the shield of safe-harbour immunity. It places all downstream parties on notice that the asset is disputed and that the foundational debt has been reconciled at the U.S. Treasury, converting any further dealing in the asset—such as pursuing foreclosure—into an act of conversion and fiduciary fraud.

This dispute fundamentally relies on the severe statutory obligations imposed upon the Indenture Trustee in its capacity as the central payor and transfer agent for the securitized pool. As an indentured trustee operating within global securitization markets linked to U.S. clearing facilities, the trustee is strictly bound by the federal provisions of the Trust Indenture Act of 1939 (TIA). A detailed audit of the securitization pipeline reveals two distinct, systemic violations of the TIA:

1. Fiduciary Neglect under TIA § 315(c): Section 315(c) imposes a strict "prudent person" standard of care on the trustee during an event of default. It requires the trustee to exercise the rights and powers vested in it with the same degree of care and skill as a prudent person would exercise in the conduct of their own affairs. Having been served a formal Notice of Adverse Claim and empirical evidence of the Treasury-level 1099-OID discharge by the 98-series trust, the indenture trustee is legally obligated to independently investigate the securitization chain and halt unperfected enforcement actions by its servicing agents.

2. Impairment of Rights under TIA § 316(b): The cornerstone of the litigation strategy rests upon TIA § 316(b), which explicitly protects the absolute, unimpaired right of a holder of any indenture security to receive payment of principal and interest, and to institute suit for the enforcement of such payment. Section 316(b) strictly prohibits non-consensual amendments or impairments to core payment terms. Because the foreign grantor trust has established itself as the true Holder in Due Course, the pursuit of an out-of-court or local foreclosure by a servicing nominee—while concurrently suppressing the U.S. Treasury-level discharge of the debt—constitutes an unlawful, non-consensual impairment of the trust's absolute rights.

To Read More: