WHY TRUST THE CLIFFORD PROTOCOL? | FOUNDATION OF MODERN CREDIT | HJR 192 AND THE 1933 MONETARY REORGANIZATION | ABANDONED CREDIT TAX RECOUPMENT UNDER IRS 1212

11th March 2026

The Jurisdictional Foundation of Modern Credit: HJR 192 and the 1933 Monetary Reorganization

The contemporary financial architecture is fundamentally predicated on the formal bankruptcy and insolvency of the United States Federal Government, an event initiated by the Emergency Banking Act of March 9, 1933. This state of emergency catalysed a radical reorganization of the global monetary system, culminating in the passage of House Joint Resolution 192 (HJR 192) on June 5, 1933. To understand the fiduciary recoupment protocols managed by Ecclesia Trustees, one must grasp the technical shift from a system of "payment" to a system of "discharge" established by this resolution.

As noted in the legacy lectures of legal researcher Jean Keating, HJR 192 abrogated the "gold clause" in all contracts, declaring it against public policy to require payment in any specific "kind of coin or currency". This effectively removed gold and silver—the traditional "good and valuable consideration"—from the private sector. Because HJR 192 removed the substance required to pay, the law established a mandatory system of "discharge" where obligations are balanced "dollar for dollar" using Federal Reserve Notes (FRNs). These notes are not money in the traditional sense; they are debt obligations of the United States Treasury.

The removal of the people's gold created a usufruct relationship, wherein the government borrowed an interest in everything the citizens create, establishing a usufruct interest in their labour, estates, land, and businesses. Consequently, all debts in the public sector are technically prepaid with the credit created from the people and their property.

Professional Career of Iain Clifford: The INTJ Architect

The professional trajectory of Iain Clifford (also referred to as Iain Clifford Stamp) is characterized by high-level mastery of wealth management, financial engineering, and systemic risk analysis spanning over forty years. Clifford is identified by forensic analysts as an "INTJ brain type," a strategic classification describing a mindset capable of solving complex, multi-layered financial problems through long-range systems analysis and contingency planning.

Chronological Career Overview

• Foundational Years (1984-1991): Clifford began his career in wealth management in the mid-1980s, pivoting from an early aspiration in professional football following a severe car collision that resulted in significant spinal injuries.

• Independent Financial Solutions (1991): He established IFS, a wealth management partnership that remains operational to this day, specializing in life insurance and asset management.

• Integrity Financial Solutions (1999-2010): Operating with direct permissions from the Financial Services Authority (FSA), Clifford built one of the largest independent wealth management firms in Southern England. The firm reached a peak independent valuation of £120 million and was recognized by the Royal Bank of Scotland (RBS) as the most profitable company in its sector.

• Technical Innovation & Consultancy: Following 2010, Clifford developed software-driven solutions, including 125 FX algorithms and the UKITI platform, which facilitated compliant pension transfers for over 100,000 users.

Educational & Regulatory Credentials

Clifford’s expertise is anchored in professional validation through the Chartered Insurance Institute (CII), where he achieved qualifications with distinction in wealth and money management, pensions, life insurance, trusts and tax. He further augmented his expertise by completing extensive research into exnihlo credit creation, securitisations and indentured trustee act.

Notable Designs

Over the course of his career, Iain Clifford has designed and implemented numerous high-level financial, trading, and fiduciary frameworks. His notable designs include:

• Maximizer Wealth Management Programs: A suite of 12 wealth management programs developed and promoted through wealth management firms and backed by HBOS via joint venture. All plan designs, structured to achieve a wide range of financial planning objectives, were designed by Iain Clifford.

• Safe Home Income Plan: Commissioned by Saga in the year 2000, this framework provided a way of using life insurance with-profit bonus rates and an arbitrage between the rate of appreciation of with-profit bonus rates and credit line costs.

• The Longevity Model: A model that solved the pension deficit via pools of US life settlement policies, creating an 8% to 10% annual cash flow yield. This enabled pension schemes to offload the longevity risk of their pension deficits through the positive cash flows of life insurance portfolios, which were promoted by listed bonds. This design went on to raise $20 billion in the US market.

• CVaR Volatility: A methodology used in the trading of 3,500 ETF funds that selected the ideal portfolio and managed the portfolios on a volatility basis designed to provide a greater return at lower risk and cost to the £billions invested in private pensions. Similar to the Scalable Capital model, this methodology has gone on to reach $5 billion in funds under management.

• 125 FX Algorithms: The development of a portfolio of 125 algorithms to trade the FX markets in a mathematically controlled volatility grid system, which consistently generated a 2% per month yield with very low drawdown.

• SOCCEREDGE: The development of an institutional-grade sports trading algorithm that trades 65 football leagues across six markets. It is self-learning and based on mathematical calculations identifying where bookmakers have historically overpriced the odds. The algorithm is similar to those developed by Tony Bloom of Brighton Football Club and Matthew Benham of Brentford Football Club.

• The Great Escape Protocols: The development of the Clifford Protocol and portfolio of Great Escape protocols. All of these frameworks have been developed after exhaustive research, rigorous pilot scheme testing, and subsequent rollout into actual designs.

Current Operations and Methodology of Iain Clifford

Iain Clifford conducts exhaustive and published research under the Ecclesia Law Institute. He actively presents his research on all subjects described as pseudo-law, "freeman on the land," and sovereign citizen, exposing these ideologies as fundamentally flawed. Instead, Iain presents the "Great Escape Protocols" via a series of open-source webinars, eBooks, websites, and interviews. Each of Iain's protocol designs is completely open source.

Iain is the founder of the Republic of Old Souls (ROS), a 508(c)(1)(a) non-profit ministry that receives donations to further its mission: the mastery of lawful commerce at an advanced level. Notably, Iain receives no salary or other remuneration from the ROS ministry, nor any remuneration from the Ecclesia Law Institute. Members and envoys of ROS self-direct administrative processes that aim to deliver each protocol, and there are no guarantees of success offered by the administrative service providers. To ensure strict compliance, IRS tax filings are conducted by a qualified Electronic Return Originator (ERO) via licensed software, and grantor trust services are provided by a Wyoming qualified trust company.

Furthermore, Iain exposes rogue actors that cause harm with malicious intent or gross negligence via the Equaliser Project (for example, the "empowerthepeople" syndicate). The Equaliser platform is provided free to members. Iain also openly offers a debate challenge to any sceptic via ROS media through a moderated debate format; however, no debates have ever happened as yet.

Outside of his legal and fiduciary research, Iain designed and built an institutional-quality professional football betting algorithm called "SOCCEREDGE" alongside a team of developers. Using this algorithm, Iain trades his own capital across 65 football leagues in 6 markets within the Asian bookmaker markets. The algorithm operates on a level of sophistication similar to those developed by renowned sports bettors Tony Bloom of Brighton Football Club and Matthew Benham of Brentford Football Club.

Whistleblowing and the FSA/FCA Regulatory Vendetta

The current legal and administrative challenges faced by Iain Clifford are the result of a fifteen-year "regulatory vendetta" orchestrated by the Financial Conduct Authority (FCA) and its predecessor, the FSA. This campaign was triggered by Clifford's role as a high-level whistleblower against systemic banking fraud.

The Integrity Liquidation and HBOS Reading Fraud (2010)

In 2008, Clifford identified evidence of a £1 billion fraud within the Reading branch of Halifax Bank of Scotland (HBOS) and a broader £40 billion hole in the bank’s balance sheet. The FSA forced Clifford’s firm, Integrity Financial Solutions, into liquidation in 2010—not due to market failure, but as a tactical manoeuvre to silence his knowledge of HBOS insolvency and shift compensation liabilities to the Financial Services Compensation Scheme (FSCS). This "administrative laundering" allowed the regulator to protect tier-one banking interests while dismantling a firm whose principals were whistleblowers.

Arck Estrella and Institutional Inaction (2011-2015)

In 2011, Clifford provided the FSA with a detailed forensic report on the Arck Estrella Ponzi scheme. Despite receiving the intelligence necessary to freeze assets, the regulator remained paralyzed for four years, resulting in over £50 million in avoidable investor losses. The FCA subsequently pivoted its investigation to target Clifford in a retaliatory campaign for his initial whistleblowing.

Parliamentary Censure of the FCA

The All-Party Parliamentary Group (APPG) on Investment Fraud confirmed Clifford's assertions of regulatory bad faith in reports published between 2024 and 2025. The APPG concluded that the FCA is "incompetent at best, dishonest at worst," citing a culture of institutional bias where the regulator is "culturally and economically aligned" with large banks and authorized firms.

Republic of Old Souls: Ministry Status and Religious Protection

The Republic of Old Souls (ROS) operates as a dedicated ministry, asserting that the commercial doctrines it teaches—concerning credit recoupment and jurisdictional autonomy—are protected religious and philosophical beliefs. Under the "Equaliser Redress Protocol," the ministry maintains that its members and envoys are entitled to believe in and execute the Clifford Protocol and other administrative pathways devised by Iain Clifford.

Any attack, character assassination, or defamatory reporting by journalists or bloggers targeting ROS members or envoys is classified by the ministry as an infringement of religious beliefs and institutional malfeasance. Such actions will be prosecuted via the Equaliser Redress Protocol to hold secular actors accountable for the systematic suppression of a religious movement and the violation of the right to a fair trial under Article 6 of the ECHR and Article 1 of the US Constitution.

The Technical Reality of Credit Creation: Werner and the Bank of England

Justification for the fiduciary recoupment of credit energy is supported by modern economic data from the Bank of England and the research of Professor Richard Werner. In his seminal papers, "How do banks create money?" and "Can banks individually create money out of nothing?", Werner empirically demonstrates that banks do not lend pre-existing deposits. Instead, they create credit ex nihilo ("out of nothing") by monetizing the borrower's signature.

The Bank of England’s 2014 report, "Money in the Modern Economy," confirms this, stating that 97% of the money supply is created by commercial banks through the act of lending. When a man or woman signs a mortgage or loan agreement, they are the true originator of the credit. Under the Bills of Exchange Act 1882, these signed documents are negotiable instruments. The bank merely acts as a nominee or withholding agent, discounting the instrument and securitizing it into products with CUSIP numbers. This process generates Original Issue Discount (OID) income—the difference between the issue price (zero at signature) and the redemption price.

Nominees and the Securitization of the Signature

In the architecture of modern commercial finance, a "nominee" is an entity that holds legal title to a financial instrument, property, or account for the benefit of another party, who remains the true beneficial owner. When a living man or woman signs a promissory note or loan agreement, they are the true source and originator of the credit generated by that signature.

However, the originating banks and subsequent investment banks do not hold these instruments as the true creditors. Instead, they act as nominees. During the securitization process, the private negotiable instrument (the signature) is monetized, pooled, and transferred to investment banks where it is assigned a CUSIP number for trading on the secondary market. The investment banks hold these securitized instruments in omnibus accounts under "street names."

In this capacity, the banks serve as nominees or withholding agents capturing the Original Issue Discount (OID) income generated by the living soul's securitized signature. Because they act as nominees, they are statutorily required under IRS Publication 1212 to report this income and remit backup withholding to the

U.S. Treasury. The banks are merely administrative middlemen facilitating the trading and reporting of the asset; they do not own the underlying credit energy generated by the signature.

Securitization of Debt Instruments by Investment Banks

Modern investment banks operate a global "nominee architecture" where private negotiable instruments are monetized and traded as standardized securities.

The Trust Indenture Act of 1939 and CUSIP Tracking

Under the Trust Indenture Act of 1939, investment bank indentured trustees hold legal title to these bundled assets for investors while acting as nominees for the true creditors (the signers). These instruments are assigned CUSIP numbers, allowing them to be tracked and traded globally.

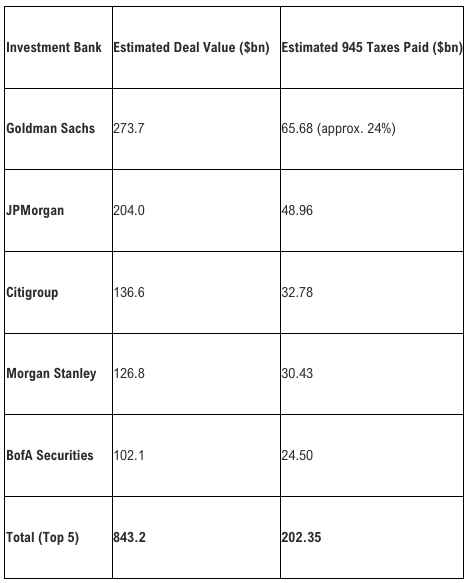

Omnibus 945 Tax Filings and Estimated Values

Because investment banks manage the trading and distribution of Original Issue Discount (OID) income, they are required by law to file Form 945 (Annual Return of Withheld Federal Income Tax) under their own omnibus accounts. This reports backup withholding on the abandoned credit energy generated by the living soul.

Forensic estimates based on the 2025/2026 M&A and CLO Advisor Rankings suggest the following values for securitizations and their corresponding 945 tax pools:

Lawful Redirection of 945 Taxes via 98-Series Grantor Trusts

The success of the Clifford Protocol lies in satisfying the IRS matching algorithm by redirecting taxes paid by nominee payers back to the true beneficial owner.

Redirection Logic

Investment banks fund the IRS taxes under their 945 tax modules as nominees. However, because the living man or woman originated the credit, the 98-Series International Grantor Trust—acting as the Holder in Due Course (HDC)—is the lawful recipient of that withheld credit. By filing a corrective 1099-OID identifying the bank as the nominee, the Trust diverts these abandoned taxes from the bank's omnibus account to the Trust's private ledger. The recruitment of abandoning credit makes no difference to the banks because they're already paying taxes under their Omnibus 945 modules. The recruitment is a redirection of the taxes to the true creditors via the holder in due course.

Definition: Holder in Due Course (HDC)

Under the Bills of Exchange Act 1882 and UCC § 3-302, a Holder in Due Course is a person or entity that acquires a negotiable instrument for value, in good faith, and without notice that it is overdue, has been dishonoured, or is subject to any defence or claim. An HDC holds the instrument free from most defences that the parties to the original transaction might have against one another. The 98-series trust establishes this status by taking legal title to the original promissory note originated by the grantor.

IRS Verification and Transparent Bank Sign-Off

Every single Grantor Trust nominee filing is confirmed with the IRS by the professional practice line. The verification of the amount of the recoupment is therefore verified for each trust before any Form 1041 tax return is submitted. Furthermore, the entire process is also signed off by the investment banks and by the trustee custodian banks that receive the ACH and Fedwire transfers from the IRS. The whole process is conducted with complete transparency to the banks receiving the ACH and Fedwire, with the Ecclesia Trustees having conducted a professional verification of each recoupment with the IRS via the IRS professional practitioner line.

The receipt of recoupments is managed via master and sub-account structures following full deep due diligence by a portfolio of US Banks that work with Ecclesia Trustees. These institutions have satisfied all compliance requirements through the application of the Clifford Protocol, a process that is 100% in compliance with the IRS system.

Forensic Anatomy of the 1099-OID and Publication 1212 Compliance

A central pillar of the fiduciary defence is the "Nominee Reporting Mandate" found in IRS Publication 1212. A courtroom-ready justification relies on the following paragraph:

"A critical component of Publication 1212 is the definition and reporting requirement of a 'nominee.' If a party holds an OID instrument but is not the true owner, that party is considered a nominee. If a nominee receives a Form 1099-OID that includes amounts belonging to another person, the nominee is required by law to file a corrective Form 1099-OID to show the proper distribution of the OID and any withheld tax to the actual beneficial owner. This 'nominee correction' is a standard ledger adjustment used by professional clearing houses and brokerages to reconcile omnibus accounts".

The Colaco and Goldberg Paradigms: Fatal Errors in Debtor Filings

The fraud models promoted by Franzie Colaco and Simon Goldberg were forensically flawed because they did not understand IRS Publication 1212 or the role of nominees. They attempted to file as taxpayers or debtors using Social Security Numbers (SSN) rather than establishing proper fiduciary capacity.

Case Study: United States v. Franzie Colaco (2014)

As confirmed by the news report from the Western District of Washington, Franzie F. Colaco was sentenced to nine years (108 months) in federal prison for orchestrating a massive 1099-OID fraud scheme. Colaco conspired with Ronald L. Brekke to convince individuals that they could claim U.S. tax refunds equal to the value of their personal debts.

• Total Tax Loss: Refund claims totalling approximately $14 million were paid to followers before detection.

• Restitution: Ordered to pay $6,206,998 to the IRS.

• Fatal Flaw: Two-thirds of the filers were Canadians who filed as SSN/ITIN recipients. By filing under an SSN, they stood in a Subject/Debtor capacity. By definition, a taxpayer owes the IRS; the IRS does not owe the taxpayer "commercial energy".

Case Study: Simon Goldberg Syndicate

Simon Goldberg instructs UK residents to file IRS Form 1099-OID claiming everyday consumer spending is US-source income with 100% tax withheld. Like Colaco, Goldberg utilizes the "Birth Certificate construct"—filing as the Debtor via an ITIN. This triggers automatic TC-810 Refund Holds because the recipient claims a refund for an amount greater than what the payer has deposited in their 945 modules.

Broad Overview of 1099-OID Federal Convictions

Other defendants were jailed for identical errors, failing to assume the role of HDC through a separate 98-series fiduciary entity:

• United States v. Anderson (2011): Convicted for filing 1099-OID forms claiming mortgage payments were "withheld income". The court ruled this was a fraudulent attempt to discharge personal debt.

• United States v. Heath (2014): Attempted to reclaim "abandoned funds" via SSN-based filings. The prosecution argued that because the filings were made under the individual's personal tax identity, they constituted a "false claim against the United States."

Conclusion: Synthesis of Fiduciary Recoupment vs. Criminal Fraud

The comparative analysis demonstrates that 1099-OID success is achieved only through data reconciliation and the assertion of fiduciary standing. By referencing IRS Publication 1212, the Bills of Exchange Act 1882, and the economic research of Richard Werner and the Bank of England, a fiduciary established as an HDC can provide a sound basis for redirecting abandoned national credit back to the private treasury of the living soul. ROS member trusts have received approximately $600 million in IRS confirmations via the Clifford Protocol, establishing the 98-series methodology as the only lawful pathway for credit recoupment.

Sources and References

• U.S. Department of Justice Press Release (Visual Context): "Scheme Caused $14 Million Tax Loss, Enriching Defendant By More Than $600,000," detailing the 9-year federal prison sentence, $6.2 million restitution, and $14 million tax loss associated with the Franzie F. Colaco 1099-OID fraud scheme.

• Internal Revenue Service (IRS) Publication 1212: "Guide to Original Issue Discount (OID) Instruments," defining the reporting requirements for nominees holding OID instruments on behalf of true owners.

• Bank of England Quarterly Bulletin (2014): "Money in the modern economy: an introduction" by Michael McLeay, Amar Radia, and Ryland Thomas, detailing how banks create credit ex nihilo.

• Academic Economic Research: Werner, Richard A. (2014). "Can banks individually create money out of nothing? — The theories and the empirical evidence" and "How do banks create money, and why can other firms not do the same?" International Review of Financial Analysis.

• Statutory Frameworks: The Bills of Exchange Act 1882 and the Trust Indenture Act of 1939, establishing the rules for negotiable instruments and the duties of indentured trustees.

• Federal Case Law: Court records and DOJ releases detailing convictions for "Strawman" or "Debtor" 1099-OID filings, including United States v. Anderson (2011), United States v. Brekke (2013), and United States v. Heath (2014).

• Ecclesia Law & MLITR Research LLC Internal Reports: Fiduciary mandates, transcript reconciliation protocols, and comparative analyses of the Clifford Protocol vs. fraudulent syndicate operations.

• Jean Keating Legacy Lectures: Historical analysis of HJR 192, the 1933 monetary reorganization, and the transition to a discharge-based credit system.

Works Cited

1. Guide To Original Issue Discount (OID) Instruments: Publication 1212 | PDF | Bonds (Finance) | Withholding Tax - Scribd, accessed on March 10, 2026, https://www.scribd.com/doc/312797357/p1212

2. Money-in-the-modern-economy-an-introduction.pdf

3. Publication 1212 (Rev. December 2013) - IRS.gov, accessed on March 10, 2026, https://www.irs.gov/pub/irs-prior/p1212--2013.pdf

4. Canadian Promoter of Tax Fraud Scheme Sentenced to Nine Years in Prison, accessed on March 10, 2026, https://www.justice.gov/usao-wdwa/pr/canadian-promoter-tax-fraud-scheme-sentenced-nine-years-prison