"THE SPANIARD" (SIMON GOLDBERG) | YouAndYourCash & EmpowerThePeople

DEBT SETTLEMENT RESULTS Vs THE REALITY OF FIDUCIARY RECOUPMENT

1. Executive Summary

This report provides a forensic analysis of the debt discharge methodology promoted by Simon Goldberg (known as "The Spaniard"), operating under the brands YouAndYourCash, WhiteRabbitTrust and EmpowerThePeople.

The subject's marketing displays numerous "wins" against high street banks (Lloyds, Barclays), debt collectors (Capquest, Marstons), and councils. Ecclesia Law classifies this strategy not as "Debt Discharge" in the lawful sense, but as Aggressive Administrative Attrition. The "successes" are largely commercial write-offs where creditors abandon claims not because the debt is invalid, but because the cost of litigating against a persistent, sophisticated "nuisance" defendant outweighs the potential recovery. While effective for low-value/unsecured debt, it is a high-risk strategy that relies on the creditor's apathy rather than the debtor's standing.

2. The Methodology: "The Spaniard's" Approach

Based on the video evidence and case files presented by White Rabbit Trust, the methodology operates on a "Combatant" model involving intense procedural resistance. Ecclesia Law is a trading style of MLITR Research LLC, Wyoming, USA. Ecclesia Law operates exclusively under Attorney-in-Fact mandates granted by its clients through private powers of attorney, trust indentures, fiduciary appointments, and private contracting structures.

A. The "Three Pillars" of Attack

1. The Paperwork Blizzard: Goldberg utilizes a dense sequence of notices, likely including Data Subject Access Requests (DSARs), Notices of Estoppel, and Copyright/Fee Schedules. The goal is to burden the creditor's legal department with so much compliance work that the file becomes "toxic."

2. Challenge of Contract (The "Wet Ink" Argument): The strategy persistently demands the original "Wet Ink" contract or the Deed of Assignment (for sold debts). While legally a copy is often sufficient under the Consumer Credit Act, many debt buyers (like Capquest) do not hold the original paperwork and will fold if pressed hard enough.

3. "Without Prejudice" Settlements: A key feature of Goldberg's "wins" (e.g., the Marstons case) is the negotiation of a "Full and Final Settlement" for a fraction of the debt. The letters often explicitly state the creditor is settling "purely on a commercial basis" to avoid further costs.

B. The "EmpowerThePeople" Platform

This platform essentially industrializes the "Freeman" arguments, providing users with templates to act as their own "Advocates." It frames the struggle as a fight against a corrupt system, encouraging users to play a game of "chicken" with bailiffs and solicitors.

3. Analysis of "Successes": Why They Win (The Commercial Reality)

The video evidence (e.g., Marstons Holdings letter) provides the "smoking gun" for why this method appears to work.

• The "Overriding Objective": In the Marstons letter shown in the video, the creditor's legal team explicitly cites the "Overriding Objective" (Civil Procedure Rules). This rule requires courts to deal with cases "proportionately."

• The Calculation: If Goldberg helps a client create 50 hours of legal work for a £1,500 council tax debt, the creditor will spend £10,000 in legal fees to recover £1,500.

• The Result: The creditor issues a Notice of Discontinuance or accepts a low settlement (e.g., £1,500 on a larger claim) simply to close the file.

• The Optical Illusion: Goldberg presents these letters as proof that "The Debt Was Fake." In reality, the letter proves "The Defence Was Too Expensive to Fight." The creditor ran a cost-benefit analysis and walked away.

4. The Fundamental Flaws: Why It Is Not "Remedy"

A. Commercial Write-Off vs. Lawful Discharge

• The Flaw: Getting a bank to "write off" a debt is not the same as discharging it. A write off often leaves a Default on the credit file for 6 years, ruining the individual's financial capacity.

• The Tax Trap: In some jurisdictions, a forgiven debt is considered "Cancellation of Debt Income" and can generate a tax liability.

• The Zombie Debt Risk: Often, a bank will "close the file" only to sell the debt to a more aggressive junk-debt buyer who ignores the previous correspondence, restarting the war.

B. The "Combatant" Status

• The Flaw: This method requires the user to remain in the jurisdiction of the court as a belligerent defendant. They are "playing the game" (as the videos say).

• The Danger: If a creditor does decide to make an example of the user (often done with high-value mortgages), these "template defenses" collapse in court. Judges routinely strike out "wet ink" and "strawman" arguments as "totally without merit," leading to immediate summary judgment and heavy cost orders.

C. Lack of Recoupment

• The Flaw: Goldberg's method saves the user money by avoiding payment, but it does not Recoup the Credit. The user remains a debtor who "got away with it," rather than a Creditor who balanced the account. They leave the Original Issue Discount (OID) unclaimed in the bank's 945 module.

The only peaceful and functional remedy that does not destroy the credit score follows this specific fiduciary cycle:

- Establish the Fiduciary Nominee (Asset Fortress Protocol): The Living Man must cease acting as the "Debtor" (Strawman) and establish a 98-Series International Grantor Trust. This Trust acts as the Holder in Due Course and the Fiduciary Nominee for the living estate.

- Target the 945 Module (Source of Funds): The Trust identifies the specific financial institution (Bank) that monetized the user's signature. It targets the Bank's IRS Form 945 Tax Module, where the withheld Original Issue Discount (OID) funds are pooled.

- File 1099-OID for Recoupment: The Trust files a 1099-OID as the Payee, naming the Bank as the Payer. This filing instructs the IRS to correct the nominee reporting error (per IRS Publication 1212) and move the "abandoned credit" from the Bank’s 945 pool to the Trust’s EIN.

- Recoup to the Asset Fortress: The Treasury/IRS releases the credit (refund) to the Asset Fortress Protocol (AFP), effectively "funding" the private treasury with lawful commercial value.

- Discharge the Liability: The AFP now holds liquid funds. It uses these funds to discharge the original debt (mortgage, tax, fine) via lawful Third-Party Settlement.

- Recoup the Discharge (The Cycle): Because the discharge payment was also a securitizable event (spending credit/energy), the Trust can file a subsequent OID claim on that transaction. This allows the AFP to recoup the cost of the discharge, creating a sustainable cycle of credit management.

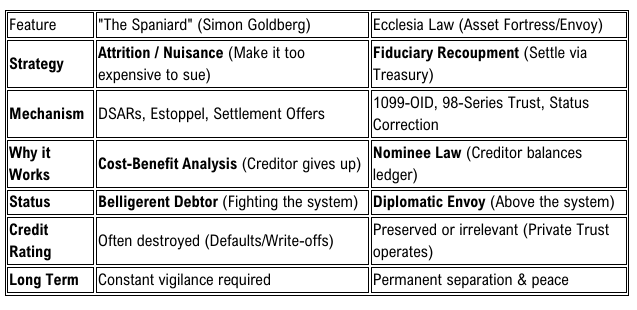

5. Conclusion & Comparison

Ecclesia Law Verdict: Simon Goldberg's "White Rabbit Trust" offers a tactical shield for those already drowning in debt and willing to fight in the mud. It is effective at scaring off low-level predators (bailiffs/unsecured lenders) through commercial pain.

However, it is fundamentally flawed as a long-term remedy because it relies on the opponent's weakness rather than the individual's sovereign standing. It wins battles but leaves the user in the status of a "protesting slave" rather than a "free Sovereign Creditor."