THE "NO CONTRACT" FALLACY IN COUNCIL TAX DEFENSE

January 23rd 2026

Analysis of The Sovereign Project Methodology vs. Judicial Reality

1. Executive Summary

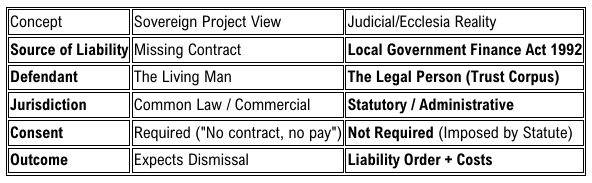

This technical paper critiques the defence strategy promulgated by Pete Stone of The Sovereign Project regarding UK Council Tax liability. The specific strategy involves demanding a "contract" from the Local Authority and arguing that the absence of a signed agreement negates liability.

Ecclesia Law classifies this strategy as a Category Error. It attempts to apply Private Contract Law principles to a Public Statutory Obligation. In a courtroom setting—whether Magistrates, County, or High Court—this argument fails because it fundamentally misunderstands the source of the Council’s authority and the legal status of the defendant. The following analysis details why this approach results in summary judgment against the defendant and outlines the judicial mechanisms used to dismantle it.

2. The Sovereign Project Hypothesis

The strategy teaches that:

1. Council Tax is a service.

2. Services require a contract (offer, acceptance, consideration).

3. Because the resident never signed a contract with the Council, there is no "meeting of the minds."

4. Therefore, the resident can stand in court and declare, "I have never seen the contract, and I cannot be bound by an invisible agreement."

3. The Judicial Response: Three Fatal Flaws

When this argument is presented in a High Court or Magistrates Court, the Judge will invariably reject it based on three specific legal realities. As noted, proponents like Pete Stone cannot point to a single binding precedent where this argument has succeeded.

A. The Absence of Precedent (Stare Decisis)

• The Judicial Challenge: The Judge will ask, "Mr. Stone, can you cite a single case precedent where a Council Tax liability was voided because the occupant did not sign a contract?"

• The Reality: There is no such case law. The courts (High Court and Court of Appeal) have consistently ruled that "Freeman-on-the-Land" arguments regarding contracts are "without legal foundation."

• The Consequence: By failing to provide precedent, the defendant is asking the court to overturn centuries of established public law based on a personal theory. The court will strike this out as "frivolous and vexatious."

B. Statutory Obligation vs. Contractual Consent

• The Judicial Challenge: The Judge will state, "The Council is a statutory body operating under the Local Government Finance Act 1992. It does not require your consent to levy a tax; it requires only your status as a resident."

• The Reality: Taxes are not commercial contracts; they are unilateral impositions created by legislation.

o Private Law: Requires consent (Contract).

o Public Law: Requires jurisdiction and status (Statute).

• The Consequence: Arguing "I didn't agree to this" is legally irrelevant. It is akin to arguing "I didn't agree to the speed limit." The obligation arises from the Act of Parliament, which applies to all subjects within the jurisdiction, regardless of individual assent.

C. The "Body Corporate" and Agency (The "Strawman" Reality)

• The Judicial Challenge: The Judge will identify that the tax bill is addressed to the Legal Person (e.g., MR JOHN DOE), not the living man.

• The Reality: The "Legal Person" (created via the Birth Certificate registration) is the property of the Crown/State.

o The Crown has the absolute right to tax its own property (the Legal Person).

o When the living man stands in court to argue, he is presumed to be the Agent or Surety for that Legal Person.

• The Consequence: It is irrelevant whether the living man saw a contract. The entity being taxed (the Legal Person) is a creation of the State. By answering to the name and arguing the case, the living man accepts the role of Surety. The State does not need the Surety's permission to tax the Principal (the Legal Person).

4. Ecclesia Law Technical Analysis

The failure of the Pete Stone strategy lies in its inability to distinguish between Commercial Law and Trust/Statutory Law.

The "Unjust Enrichment" Factor

Even if the court entertained a contract theory, they would apply the doctrine of Implied Contract or Unjust Enrichment. By occupying a property that benefits from Council services (roads, lighting, police, waste), the occupant is deemed to have accepted the benefit. In Equity, he who accepts the benefit must accept the burden. Denying the contract while consuming the service is viewed as fraud.

5. Conclusion: The Correct Pathway

The Pete Stone argument is a functional fallacy. It attempts to use a commercial defence (missing contract) against a statutory imposition.

Ecclesia Law Verdict: To lawfully avoid Council Tax, one cannot argue contracts inside the court. One must remove the standing that attracts the tax.

1. Do not argue the contract. Admit the statute exists but prove it does not apply to you.

2. Status Correction (Envoy Protocol): The liability attaches to the "Resident" (a statutory definition). By correcting status to that of an Ecclesiastical Envoy or Foreign National, and placing the property into a Private Trust (Asset Fortress Protocol), the individual removes the "Resident" status.

3. Jurisdictional Severance: If there is no "Resident" in the statutory sense, the Local Government Finance Act 1992 has no subject matter jurisdiction.

4. Or better still discharge the council tax from your Asset Shelter Protocol treasury and recoup it.

This is a status correction strategy, distinct from the failed contract dispute strategy offered by The Sovereign Project.