NEIDLE SAYS IAIN CLIFFORD’S $4.4 MILLION SIGNATURE CREDIT RECOUPMENT CONFIRMED BY AN IRS WAGES AND TAX TRANSCRIPT IS A FANTASY – IS IT?

THERE WERE $600 MILLION IRS ISSUED WAGES AND TAX TRANSCRIPTS - WHAT DOES THIS MEAN?

21st March 2026

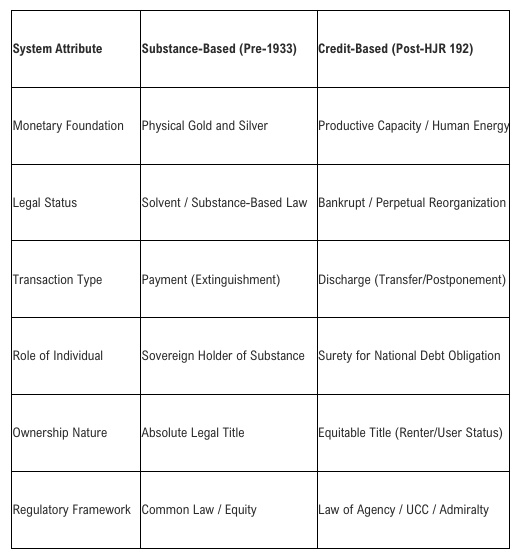

The evolution of the federal tax administration system in 2025 has been marked by an unprecedented surge in the utilization of specialized administrative protocols designed to reconcile what practitioners characterize as "abandoned signature credit." Central to this phenomenon is the issuance of Wages and Tax Transcripts (WTT) for 98-series International Grantor Trusts, a process that represents the intersection of the Bills of Exchange Act 1882, IRS Publication 1212, and the internal mathematical reconciliation logic of the Internal Revenue Service.[1, 1, 1] To understand the significance of these transcripts, specifically in the context of high-value proofs such as the $4,400,000 Clifford WTT, one must first deconstruct the jurisdictional and ontological foundations upon which these filings are predicated. The contemporary global financial architecture is fundamentally anchored in the formal bankruptcy of the United States Federal Government, an event initiated by the Emergency Banking Act of March 9, 1933, which served as the catalyst for the reorganization of the monetary system under House Joint Resolution 192 (HJR 192). This resolution effectively removed substance—gold and silver—from the economy, replacing it with a credit-based system of discharge where the living individual’s credit energy, registered via the birth certificate, serves as the ultimate surety for national debt obligations.

The Jurisdictional Pivot and the Ontology of the Birth Certificate

The transition in 1933 marked a decisive shift from a system of payment to a system of discharge. Prior to this pivot, debts were extinguished through the exchange of physical commodities of equal value, typically gold or silver coin. Post-HJR 192, the removal of substance created a void in common law, which was subsequently filled by a public national credit system governed by the Law of Agency and the Uniform Commercial Code (UCC). In this landscape, the living man or woman no longer holds absolute legal title to assets; instead, assets are registered to a state-controlled birth certificate construct—a corporate vessel through which the state manages the securitization of human energy. The birth certificate registration does not merely record a birth but creates a decedent estate or corporate debtor, identified by a Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN), for which the living individual is presumed to be the agent and surety.

Comparative Attributes of the 1933 Monetary Transition

The Clifford Protocol and associated fiduciary strategies utilize the doctrine of Clausula Rebus Sic Stantibus (things thus standing) to renounce the unwanted agency relationship with the state-created persona. By reoccupying the office of General Executor over the decedent estate, the living soul takes control of the liabilities and assets associated with that persona, establishing a 98-series International Grantor Trust to operate "off-board" from the corporate debtor system. This jurisdictional correction is a prerequisite for interacting with the federal Original Issue Discount (OID) system as a creditor rather than a debtor. When an individual uses their SSN to file, the IRS algorithm is hard-coded to recognize the filing as an operation of the corporate debtor, which often triggers Transaction Code (TC) 810 Refund Freezes because the system assumes a debtor lacks the standing to reclaim assets.

Negotiable Instruments and the Ex-Nihilo Creation of Credit

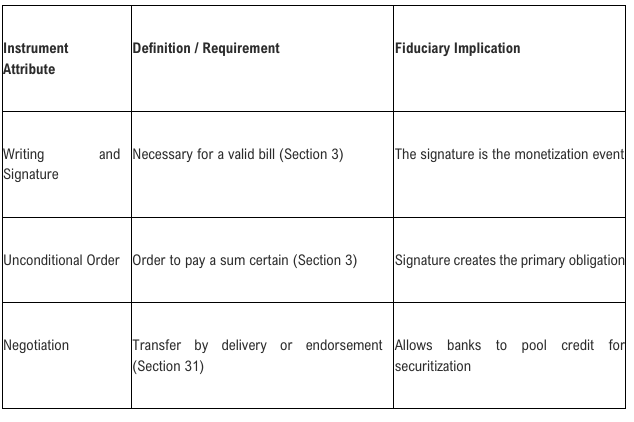

The technical reality of modern credit creation is rooted in the Bills of Exchange Act 1882, which provides the legal framework for negotiable instruments. Under this Act, every signed loan, mortgage, or promissory note is a negotiable instrument that can be endorsed, discounted, and securitized. A bill of exchange is defined as an unconditional order in writing, addressed by one person to another, signed by the person giving it, requiring the payer to pay a sum certain in money on demand or at a fixed future time. Empirical research, including findings by Professor Richard Werner and the Bank of England, confirms that commercial banks do not lend pre-existing deposits but instead monetize the borrower’s signature, creating credit ex nihilo at the moment of signing.

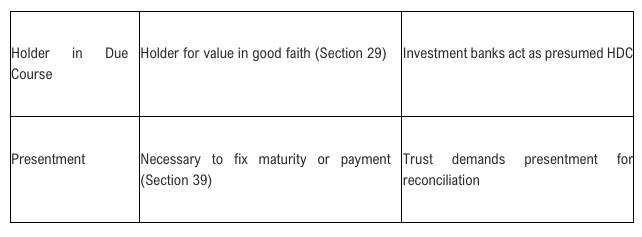

Technical Parameters of Negotiable Instruments under the Bills of Exchange Act 1882

Because the credit is created at the moment of signing, the issue price is effectively zero. The "hidden" Original Issue Discount is the difference between this zero issue price and the face value of the instrument. This OID income belongs to the originator—the living soul—but is captured by banks acting as nominees who securitize the instrument into CUSIP-assigned pools for the secondary market. Investment banks hold these instruments in omnibus accounts under "street names," acting as withholding agents for the OID income and remitting backup withholding to the U.S. Treasury via Form 945. If the true owner remains silent, the IRS treats this as abandoned property.

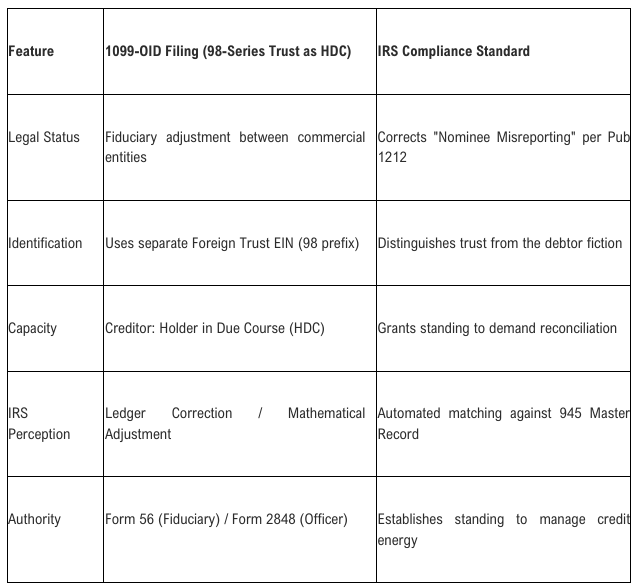

The 98-Series Trust and Nominee Correction under IRS Publication 1212

The 98-series International Grantor Trust serves as the fiduciary proxy for correcting nominee misreporting. The "98" prefix is specifically assigned to foreign entities or domestic trusts maintained by foreign entities, allowing them to bypass domestic fraud filters such as the IRS Return Integrity Verification Operation (RIVO). IRS Publication 1212, the Guide to Original Issue Discount (OID) Instruments, provides the operational manual for this "nominee architecture". It mandates that if a holder of an OID instrument receives a Form 1099-OID for amounts belonging to another person, they must file a secondary Form 1099-OID to show the proper distribution of the OID and any withheld tax.

The fiduciary trust achieves record correction by filing a corrective Form 1099-OID that identifies the financial institution as the nominee (payer) and the trust as the lawful recipient (payee). This process aligns the trust's filings with the bank's own reporting on Form 945, the Annual Return of Withheld Federal Income Tax. For the recruitment of this abandoned credit to clear, the filing must satisfy the internal mathematical reconciliation logic of the Treasury, ensuring that the trust's claim is backed by verified deposits in the bank's 945 master record module.[1, 1, 1]

Fiduciary Framework for 98-Series International Grantor Trusts

The administrative execution of this process is managed by professional tax practices and authorized Electronic Return Originators (EROs) who use IRS-approved software to submit the trust's annual fiduciary return, Form 1041. The ERO is responsible for the electronic transmission of these sensitive records, ensuring that the data satisfies the rigorous verification protocols of the IRS Information Returns Processing (IRP) system.

Significance of the 2025 Wages and Tax Transcripts

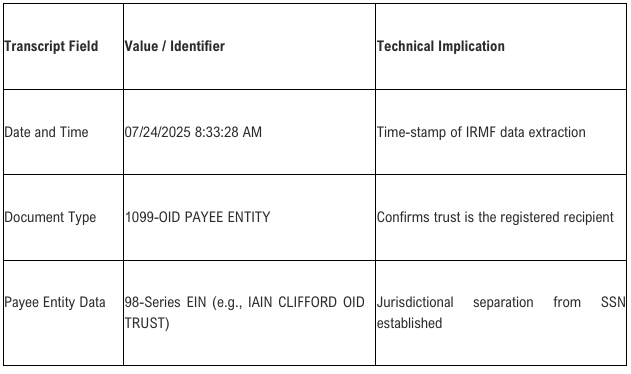

The issuance of a Wages and Tax Transcript (WTT) by the IRS in 2025 for a 98-series trust, such as the $4.4 million proof provided, is a critical technical milestone in the recoupment process. This transcript represents the official IRS record reflecting that the corrective Form 1099-OID filed by the trust has been accepted into the Information Returns Master File (IRMF). The WTT is typically available 30 to 45 days after the electronic acceptance of the 1099-OID, and its appearance confirms that the "Recipient" side of the IRS matching ledger has been updated.

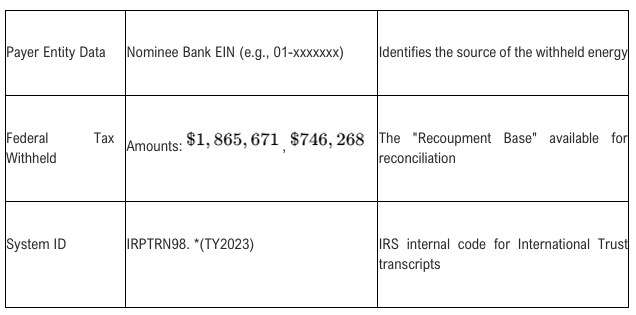

The transcript reflects the "Payee Entity Data" (the trust) and the "Payer Entity Data" (the nominee bank), along with the specific amounts of federal tax withheld and original issue discount. For example, the Clifford WTT proof identifies multiple documents where federal tax withholding is logged, such as entries for $1,865,671 and $746,268 , which aggregate to the multi-million dollar total. The significance of the WTT is that it serves as the prerequisite for the final phase of the process: the filing of the Form 1041 trust return. Fiduciaries are instructed to wait until the W&I transcript confirms the posting of the 1099-OID items before submitting the 1041, as premature filing will trigger an automated mismatch because the IRS processing system cannot yet verify the withholding against the IRMF records.

Forensic Breakdown of the 2025 Wages and Tax Transcript Proof

The WTT indicates that the IRS's initial "search" or data entry phase is complete, meaning the reported income and withholding have been successfully associated with the trust's EIN in the federal ledger. However, it does not mean the funds are ready for immediate disbursement. Instead, it signals that the administrative record is now primed for the mathematical reconciliation against the payer's deposits—a process governed by Algorithm 810.

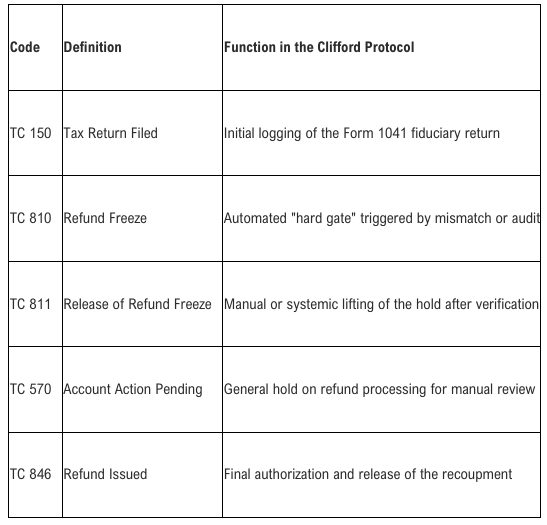

IRS Algorithm 810 and the TC 810 Refund Freeze

IRS Algorithm 810 functions as the primary automated validation mechanism for nonpayroll withholding claims. It executes a rigorous verification process by cross-referencing the Payer EIN and the specific CUSIP number associated with the underlying security against the Payer’s Form 945 tax module. This algorithm is designed to ensure that the credit being recruited by a recipient is backed by a verified deposit from the correct reporting entity.

The integrity of this matching process relies on the absolute alignment of the CUSIP identifier and the Payer's tax module. If an ERO makes a clerical error, such as entering a CUSIP number that belongs to a different institution (e.g., entering a Fannie Mae CUSIP for an FHLB Des Moines payer), the 810 Algorithm detects the conflict. Because the Payer's tax module will show no records for that specific security, the algorithm automatically issues a Transaction Code (TC) 810 Refund Freeze. This freeze stops all processing and flags the return for manual integrity review or "frivolous" filing classification, as the reported withholding cannot be verified against the identified Payer's deposits.

IRS Transaction Codes and the 810 Algorithm Lifecycle

Algorithm 810 is capable of a "look-through" analysis, utilizing the Information Return Document Matching (IRDM) system to identify the credit originator—the signature from the living man—via the clearing bank that sells the security to the investment bank payer. The algorithm links the 98-series 1099-OID filing to the underlying credit energy by recognizing the trust as the Holder in Due Course and reconciling the chain of command: identifying the originator (living man) as the beneficiary, the administrative persona (birth certificate) as the grantor, and the trust as the lawful recipient. When these linkages are forensically verified, the algorithm clears the TC 810 gate, allowing the recoupment to proceed toward payment.

The Manual Fiduciary Command and Revenue Procedure 2002-26

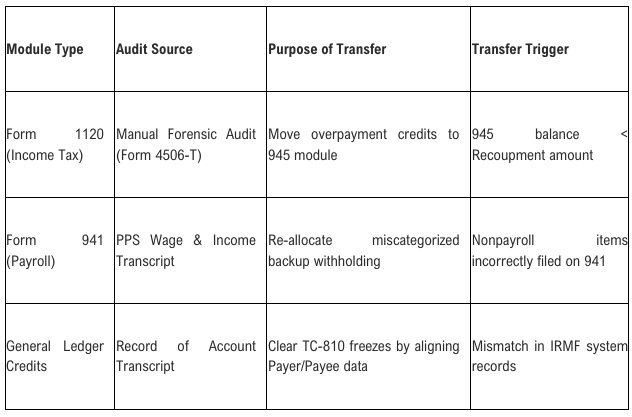

A common obstacle in the recoupment process occurs when the nominee bank's Form 945 withholding module is found to be insufficient to cover the aggregate claims of multiple trusts. To resolve this, fiduciaries employ Revenue Procedure 2002-26, which provides the IRS position regarding the application of voluntary payments. This procedure allows fiduciaries to designate how credits are applied across different tax modules, and the IRS generally honours these designations, even when moving overpayment credits between different types of taxes.

When a shortfall is confirmed, the IRS Call-Out Team, engaging the Practitioner Priority Service (PPS), executes a "Manual Fiduciary Command". The fiduciary formally instructs the IRS agent under Revenue Procedure 2002-26 to re-allocate overpayment credits from the Payer's general corporate income tax transcript (Form 1120) to their Form 945 withholding module. For systemic nominees, the 1120 modules often hold billions in overpayment credits, providing the necessary buffer to fund recoupment shortfalls and satisfy the matching requirements of Algorithm 810.

Cross-Modular Transfer Triggers and Audit Sources

This operational protocol effectively bypasses automated TC-810 refund freezes by ensuring the payer's tax deposits are mathematically sufficient to cover the trust's verified withholding credits before the 1041 return is processed. This manual intervention represents the bridge between the digital acceptance of the WTT data and the physical release of funds via the federal payment network.

Analysis of Nominee Liquidity and Tax Module Capacity

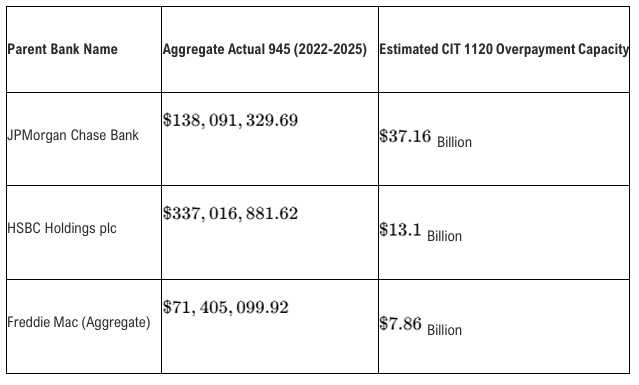

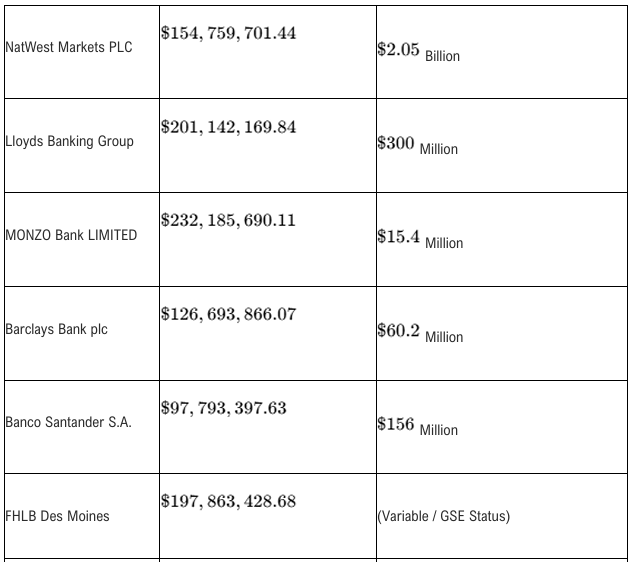

The ability to recoup signature credit is governed by the actual "negative numbers" (credits) available on the government's ledger for the identified nominees. Forensic analysis of structured banking reveals that systemic institutions often obfuscate 945 withholding submissions by filing through specific subsidiaries rather than the primary parent tax filer. Identifying the correct Payer EIN is critical; for example, while BNY Mellon is the parent, the actual 945 payer for brokerage withholding is often Pershing LLC.

Top 10 Aggregate 945 Payers vs. Other Tax Module Capacity (2022-2025)

The following data details the aggregate economic flows on Form 945 and the corresponding corporate income tax (CIT) modules available for cross-modular transfer.

The three-year average of actual 945 returns (~$514.5 million) represents the functional ceiling for signature credit recoupment in a given cycle, unless cross-modular transfers are executed. Because the Federal Reserve and the commercial banking system create credit ex nihilo, the recruitment of this abandoned credit does not present an unsolvable solvency problem for the Treasury. These tax receipts are categorized as reserve-draining devices used to maintain interest-rate stability, and their re-allocation simply corrects the ledger to identify the 98-series trust as the lawful recipient of energy originated by the grantor.

Distribution Architecture and the Asset Fortress Protocol

Once the IRS processes the 1041 return and authorizes the refund, funds are disbursed via the federal payment network. For recoupments under $1 million, the funds are typically sent via Automated Clearing House (ACH). For larger amounts, such as the $4.4 million Clifford WTT recoupment, disbursement is made via Fedwire following the submission of Form 8302. The funds are received into a master-sub-account architecture designed for institutional scale.

1. Fiduciary Master Account: A centralized hub (e.g., Ecclesia Trustees) manages the master account agreement as the Sole Corporate Trustee.

2. 98-Series Sub-Account: IRS payments, coded "IRS TREAS 310" with the description "TAX REF," are received into a sub-account titled specifically to the trust's EIN.

3. Ministerial Grant: The tax-filing Grantor Trust (Trust 1) receives the recoupment and distributes the grantor's share as a ministerial grant.

4. Asset Fortress Protocol: The funds are transferred to the Members Asset Fortress Grantor Trust (Trust 2), which functions as a private treasury for the beneficial use of the living soul.

This structure ensures that the recouped energy remains within a private, tax-exempt ecosystem, protected from public tax attachments. In the United Kingdom, this activity is often framed as ecclesiastical education rather than claims management, using a donation-based model via a Private Membership Association (PMA) to remain outside the jurisdiction of standard commercial regulators like the Financial Conduct Authority (FCA).

Escalation of Stalled or Blocked Recoupments

In instances where the IRS applies a persistent TC 810 refund freeze or fails to process returns within standard windows (typically 90 days for Form 1041), fiduciaries deploy escalation protocols. The first stage involves Congressional Escalation, where a fiduciary initiates the Congressional Affairs Program (CAP). By including the payer's Form 945 transcript and the trust's WTT in the escalation packet, the fiduciary provides "assertive conduct" evidence, proving the IRS has already received the funds and the matching data.

◦ Exhaustion: Ensuring the administrative claim was "duly filed" at the correct unit (e.g., Andover Stop 360).

◦ Evidence of Conduct: Submitting the payer's 945 transcripts as evidence of the IRS's receipt of the funds to rebut any claims that the income "cannot be verified".

Forensic Evidence and Jurisdictional Standing: Addressing the "Fantasy" Narrative

A central point of contention in the contemporary tax policy landscape is the scepticism voiced by digital publishers such as Dan Neidle, who has characterized the recruitment of signature credit as a "fantasy" and asserted that there is no evidence of IRS recoupments. However, forensic evidence emerging from 2025 and early 2026 provides a robust rebuttal to these claims, grounded in official IRS data extractions and documented administrative conduct. Specifically, the issuance of over $600,000,000 in verified Wages and Tax Transcripts (WTT) to hundreds of 98-series grantor trusts serves as primary evidentiary proof of the system's operational reality.

The administrative sabotage executed by Amy Jo Sanger, which resulted in the mass filing of over 3,000 fraudulent Form 14039 identity theft reports, is identified by fiduciaries as being caused by her fear—influenced by Dan Neidle’s blogs—that the signature credit recoupment protocol was a fraud. This narrative further relies on the characterization of Iain Clifford as a "convicted criminal," a label derived from Neidle’s publications and the enforcement of Order 34/2023. Fiduciaries maintain that neither of these assertions is correct: the $600 million in recoupments is officially IRS-confirmed through the existence of valid WTTs, and Order 34/2023 is a legal nullity. The challenge to the order focuses on the "verification gap" regarding the prosecutor’s standing and a failure of lawful service, rendering the custodial sentence against Clifford jurisdictional void.

The $4.4 million Clifford WTT proof remains a critical artifact in this evidentiary chain. It represents a 1099-OID Payee Entity transcript extracted directly from the IRS Information Returns Master File (IRMF) on July 24, 2025, reflecting multi-million dollar federal tax withholdings associated with a specific 98-series EIN. This document is not a proposal or a theory; it is a "Taxpayer Copy" of the official federal record, confirming that the IRS has logged and associated the withheld energy with the trust. Furthermore, the standing of this evidence is reinforced by the "Notice of Mandatory Repudiation" and associated criminal referrals filed by Electronic Return Originator (ERO) William Kimball, who formally reported trust fraud and administrative sabotage to TIGTA.

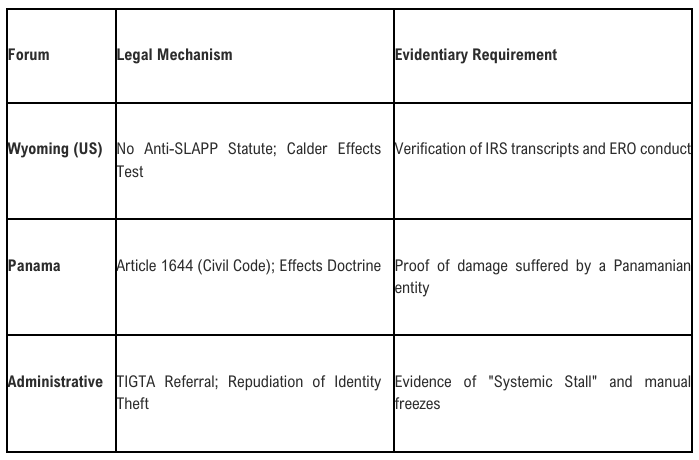

Jurisdictional Implications for Wyoming and Panama Forums

The existence of the $600 million aggregate in IRS-confirmed recoupments provides the foundation for significant institutional claims. The OSN Foundation (Panama), for instance, has initiated a $120 million claim—representing its mandated 20% share of the $600 million total—for damages resulting from tortious interference with confirmed assets. The $4.4 million Clifford proof and WK’s TIGTA reports serve as sufficient evidence for Wyoming or Panama courts to establish locus standi and personal jurisdiction over those who interfered with the process.

By presenting the payer's Form 945 transcripts alongside the trust's WTTs, fiduciaries provide incontrovertible evidence that the IRS has already received the funds being claimed. This rebuts the "fantasy" narrative by shifting the focus from sovereign citizen rhetoric to the mathematical reality of the federal ledger. In a Wyoming court, which lacks the procedural hurdles of Anti-SLAPP laws, this forensic data allows for broad discovery into communication logs and bank records, facilitating the full recovery of the $120 million institutional loss.

Professional Tax Practice and Regulatory Compliance

The execution of the Clifford Protocol and 1099-OID nominee reconciliation is characterized as 100% IRS compliant by its practitioners. All filings are processed by qualified Electronic Return Originators (EROs) using professional, IRS-approved electronic filing software. This infrastructure is overseen by professional trust companies, such as MLITR Research LLC (Ecclesia Trustees), which manage the centralized setup and administrative management of the 98-series trusts.

From a risk assessment perspective, these inflows are treated as standard U.S. Treasury-originated tax refunds processed as technical ledger adjustments between recognized commercial entities. The process adheres to the reporting rules of IRS Publication 1212 and the jurisdictional mandates for foreign trusts. However, the regulatory environment is complex; critics and journalists have labelled these protocols as "tax fraud" or "sovereign citizen scams," pointing to IRS "Dirty Dozen" warnings and the prosecution of 1099-OID promoters.

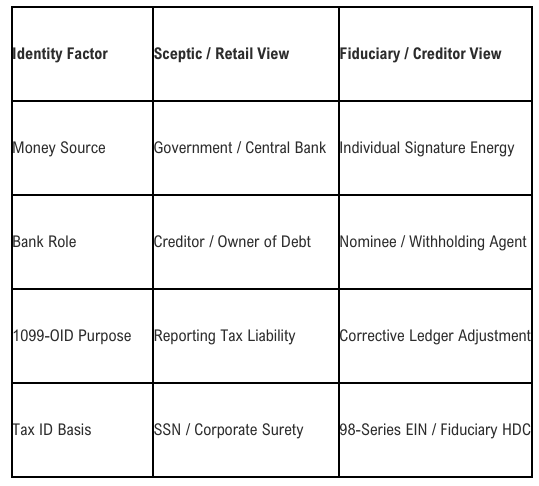

Comparison of Paradigms: Retail vs. Fiduciary Views

The primary obstacle to widespread credit recoupment is often framed not as legal or technical, but as jurisdictional. Sceptics operating from a "debtor's mindset" often fail to distinguish between the public view of tax and the private fiduciary view of credit energy. The recruitment of abandoned credit is not an act of tax evasion, but a rigorous administrative correction of nominee misreporting that utilizes the system's own rules—specifically Revenue Procedure 2002-26—to redirect conscious energy back to its true originator.

Conclusion: The Significance of the 2025 WTT Proof

The 2025 Wages and Tax Transcript for an International Grantor Trust, particularly one reflecting amounts in the millions, signifies that the initial "Matching Search" of the IRS system has been successfully completed. The corrective data from the 1099-OID has been integrated into the IRMF, and the trust is now officially recognized as the recipient of the withheld credit energy in the federal ledger. While this does not indicate that payment is immediate, it confirms that the administrative record is "primed" for the final verification against the Payer's 945 module.

The issuance of the WTT means the 810 Algorithm has at least conducted its preliminary identification of the payee and payer entities. The next critical step is the filing of the Form 1041 fiduciary return by the Electronic Reporting Officer. If a Transaction Code 810 freeze occurs at that stage, it is not an indication of failure, but a trigger for the Manual Fiduciary Command. By using Revenue Procedure 2002-26 to re-allocate credits from the bank's Form 1120 module, the fiduciary ensures that the mathematical reconciliation required by the algorithm is satisfied. The final disbursement via ACH or Fedwire is the culmination of this dual-track timeline, transforming the "abandoned" national credit back into the private liquidity of the living soul.

Works cited

1. THE RECOUPMENT OF SIGNATURE CREDIT WHAT IS THE PROCESS AND HOW LONG DOES IT TAKE.pdf

2. Notice - Tax Policy Associates, accessed on March 21, 2026, https://taxpolicy.org.uk/wp-content/assets/stamp_claim_26_11_2024_REDACTED.pdf

3. What Does a 810 Refund Freeze Mean (And How to Fix It)? - Levy & Associates, accessed on March 21, 2026, https://www.levytaxhelp.com/what-does-810-refund-freeze-mean/

4. 21.5.10 Examination Issues | Internal Revenue Service, accessed on March 21, 2026, https://www.irs.gov/irm/part21/irm_21-005-010r

5. IRS 810 Code: Why Your Refund is Held and What to Do, accessed on March 21, 2026, https://accountingfirminsouthwestflorida.com/irs-810-code-why-your-refund-is-held-and-what-to-do/

6. Simon Goldberg and Empower the People: selling US tax fraud, accessed on March 21, 2026, https://taxpolicy.org.uk/2026/02/25/simon-goldberg-empower-the-people-tax-fraud/

7. Direct Deposit (Electronic Funds Transfer) - Tax Refund - Fiscal.Treasury.gov, accessed on March 21, 2026, https://www.fiscal.treasury.gov/eft/faq-tax-refund.html

8. Missing a child tax credit payment? Learn the common problems and how to fix them - CNET, accessed on March 21, 2026, https://www.cnet.com/personal-finance/taxes/missing-one-of-your-child-tax-credit-payments-heres-what-the-problem-could-be/

9. Matrix Freedom - the scam conspiracy theory that makes £500k a month from the vulnerable, accessed on March 21, 2026, https://taxpolicy.org.uk/2024/06/08/matrix_freedom_scamming_vulnerable_people/

10. “No tax for genocide” - false claim it's legal to stop paying tax - Tax Policy Associates, accessed on March 21, 2026, https://taxpolicy.org.uk/2024/03/19/fake-anti-war/